Laying off about 50,000 people, the struggle under the sentiment of fuel vehicles: the dilemma of electrification in the European auto industry

JohnDec 11, 2024, 04:37 PM

JohnDec 11, 2024, 04:37 PM

From the Era of Fuel to the Era of Electricity: A Century of Transformation in the European Automotive Industry. The European automotive industry once led the global car manufacturing sector. However, as the wave of electrification grows stronger, why is the European auto industry struggling? Historically, European automakers were global pioneers, but now they face significant challenges. The transition from fuel-powered vehicles to electric cars is proving slow for European manufacturers. High energy costs, inadequate infrastructure, and deeply ingrained traditional thinking have all become obstacles to the electric transformation.

1. Layoffs, Pay Cuts, and Plant Closures: Volkswagen's Layoff Storm Sweeps the European Automotive Industry

If you're walking the streets of Germany today, you might still see Volkswagen employees forming protest marches. This is the largest strike at Volkswagen since 2018. On the morning of December 2, Volkswagen factories across Germany erupted in protests against the company's plans to close factories and implement large-scale layoffs. Currently, conflicts between workers and management over layoffs, pay cuts, and plant closures are escalating.

(Volkswagen employee protest team)

Recently, the union leaders of Volkswagen, the largest car manufacturer in Europe, revealed plans to close at least three factories in Germany, cut nearly 10,000 jobs, and reduce salaries by 10% in an effort to reduce costs and improve competitiveness. The announcement triggered a strike by workers at Volkswagen's factory in Zwickau, southeastern Germany, at 9:30 a.m. on December 2, marking the start of nationwide protests.

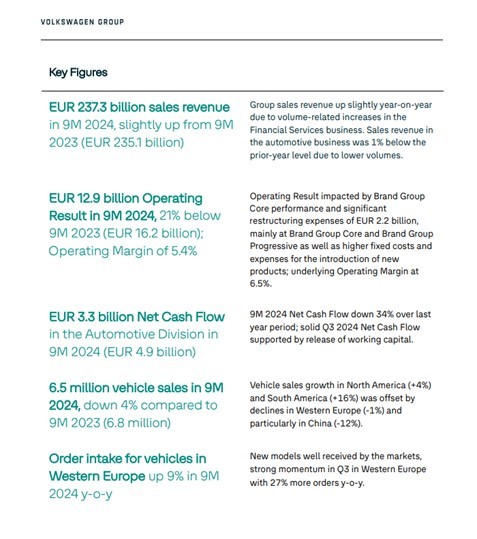

Volkswagen's layoff plans can be traced back to its recent financial report. According to Volkswagen's 2024 financial results for the first three quarters, the company posted a revenue of €237.28 billion (approximately ¥1.83 trillion), a year-on-year increase of 0.9%. However, most of the growth came from financial services, while revenues from core automotive sales declined by 1%. Notably, Volkswagen's operating profit for the same period dropped by 20.5%, amounting to €12.91 billion (approximately ¥99.7 billion). Volkswagen's labor costs are nearly double those of its European competitors, so in the face of declining profits and sluggish revenue growth, cutting costs has become the company's primary strategy.

(Volkswagen's Q3 2024 Financial Report)

If only Volkswagen were affected by the layoffs, it might be seen as a company-specific issue. However, this wave of layoffs is impacting the entire European automotive supply chain. According to incomplete statistics, a total of about 50,000 layoffs are expected across Europe, involving companies such as Volkswagen, Audi, Ford, Stellantis, and four automotive parts suppliers, including Bosch, Schaeffler, Michelin, and ZF.

(Volkswagen)

In early November, Audi announced plans to cut about 15% of its non-production workforce, affecting 4,500 jobs in Germany. On November 20, Ford stated that it would lay off 4,000 people in Europe and the UK by the end of 2027. Stellantis plans to lay off nearly 1,100 employees at its Toledo Assembly Complex in Spain starting January 5, 2024. The world's largest auto parts manufacturer, Bosch, announced plans to cut up to 5,500 jobs by 2028. French company Forvia is considering laying off 10,000 workers, or 13% of its workforce. German ZF plans to lay off up to 14,000 people by 2028. Given the scale of the layoffs, it's clear that European traditional automakers are struggling with the challenges of the electric transformation.

(Michelin Tires)

The automotive industry is not only a means of transportation but also represents national industrial development, as its supply chain involves numerous sectors. Moreover, the automotive industry is a key pillar of Europe's economy, and its turbulence will have a significant impact on the broader European economy. According to the European Automobile Manufacturers Association (ACEA), the EU's automotive industry employs 12.9 million people, accounting for 8.3% of the EU's manufacturing workforce, contributing over €390 billion in taxes, and representing more than 7% of the EU's GDP. This shows that the ongoing crisis in the European automotive sector warrants attention.

2. From Global Dominance to Market Loss: Volkswagen's Dilemma Reflects Challenges in the European Automotive Industry

When sales fail to support a company's stable revenue, businesses often look to cut costs to maintain operations. This is the direct cause of the layoffs. The main issues facing European automakers are insufficient domestic demand and losing international market share. Domestic demand in Europe is sluggish due to weak government support, high energy costs, limited charging infrastructure, and high vehicle prices. Meanwhile, European manufacturers are also losing ground to new players in the international market.

For years, the European auto industry has been a global leader, but the technological gap created by the industry's failure to adapt to electric vehicles has led to a loss of advantage. In the past, European carmakers could leverage cheap labor and resources from developing countries to profit in international markets. However, the slow pace of electrification has led to a loss of this competitive edge.

(Volkswagen Golf GTI 380)

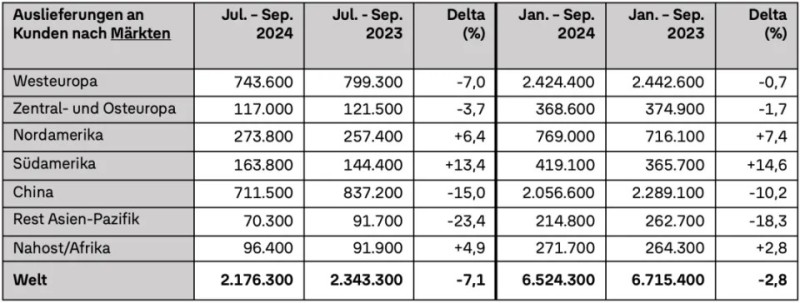

The market where this loss of share is most apparent is China. For example, China is Volkswagen's largest single market. In the first three quarters of 2024, Volkswagen's cumulative sales in China reached 2.06 million vehicles, accounting for 31.5% of the company's global sales. However, sales in this market have declined by 10.2% year-on-year, marking the steepest drop among all markets. From January to September, Volkswagen's global sales totaled 6.52 million vehicles, a year-on-year decrease of 2.8%, with the third quarter showing a 7.1% decline in sales.

(Volkswagen's global sales in each region in 2024)

Continuing with Volkswagen's data, sales in Volkswagen's other large market, Western Europe, also exhibit a declining trend. Sales in the first three quarters saw a slight decline, down 0.7% year-on-year while third quarter sales were 743,000, a decrease of 7.0% year-on-year. This indicates that Europe's capacity to absorb Volkswagen is gradually shrinking, which will directly affect the company's profitability.

Although Volkswagen's sales in its home market are declining, Toyota, a competitor, has achieved record high sales in the European market. Toyota Motor Europe (TME) delivered 912,671 Toyota and Lexus vehicles in the first nine months of 2024, an increase of 6% year-on-year, setting a new record and becoming the second-best-selling car brand in the European market, only after Volkswagen. The surge in Toyota sales may be related to the depreciation of the yen, but this is enough to prove that there is still consumer demand in the European market. Faced with Toyota's rapid growth in its home market, if Volkswagen does not respond in time, it will soon cede the first place seat.

To look at Toyota's sales data in detail, the proportion of Toyota's overall electrified models reaches 74%, and sales of electric models have increased by 7% year-on-year. Pure electric vehicle sales reached 26,824, a year-on-year increase of 19%; plug-in hybrid model sales exploded 93% year-on-year due to the launch of the Toyota C-HR PHEV. It can be seen from this that the definition of electrification is not limited to pure electric models, and the hybrid models on the international market are the ones that capture consumers' interest.

(Toyota C-HR Plug-in Hybrid)

As carbon emission standards become increasingly stringent, the European Union has mandated a ban on the sale of fuel-powered cars starting in 2035. Against this policy backdrop, traditional European automakers are facing immense pressure to transform. However, the process of electrification has been relatively slow, and sales of electric products have not been impressive. At the same time, due to the social welfare system in Europe, companies' investment in R&D personnel and production costs remain high, resulting in significant financial pressure on these companies. This situation inevitably brings to mind the transformation of traditional automakers towards fuel efficiency driven by the oil crisis, a process that was also quite bumpy.

(Volkswagen Tayron)

Although much of mainland Europe is located in higher latitudes, Western Europe, with its stronger overall consumer purchasing power, predominantly enjoys a temperate oceanic climate. As a result, the impact of low temperatures on batteries is relatively small. Among these, Norway, located in Northern Europe, also has a temperate oceanic climate and has become a pioneer in the promotion of electric vehicles (EVs) across Europe. In major cities and densely populated areas in Norway, the density of charging stations and charging points is extremely high, with charging points available every 3-5 kilometers on average. However, the primary factors affecting electric vehicle demand in Europe are still the high energy costs and the government's withdrawal of subsidies for electric vehicles.

(European Continent)

The high energy costs of electric vehicles are a significant factor contributing to the weak demand for electric cars in Europe. According to data from the German Economic Institute, the electricity cost for the German automotive industry in 2023 was 190 euros per megawatt-hour, approximately twice that of China and three times that of the United States. This high energy cost may be influenced by the supply of Russian natural gas. Against this backdrop, various European countries are continuing to tighten subsidies for electric vehicles, which results in higher car prices for consumers and weakens demand for electric cars.

Sweden canceled its electric vehicle incentives at the end of 2022. From December 2022 to January 2023, the country's electric vehicle sales immediately declined, but the market generally stabilized afterward. In the Netherlands, from 2024 onwards, subsidies for individuals purchasing new BEV (Battery Electric Vehicle) vehicles under 45,000 euros will decrease by 400 euros to 2,550 euros. As early as June 2023, the UK announced the cancellation of its 1,500-pound-per-vehicle electric vehicle subsidy program.

Taking Germany, the largest automotive market in Europe, as an example, the country ended its electric vehicle subsidy program in mid-December 2023, one year earlier than expected. When announcing the sudden cancellation of subsidies, a spokesperson for the German Ministry of Finance emphasized that the government had "no choice due to a lack of funds." In response to the resulting decline in electric vehicle sales, the German government agreed in early September 2024 to introduce measures allowing businesses to deduct part of the value of electric vehicles in their taxes.

3. System, Market, Infrastructure: Europe’s Electrification Transformation Faces Multiple Challenges

Even in the face of the EU's ban on fuel-powered cars, the transformation process of traditional European automakers toward electrification has been relatively slow. It is important to note the time lag caused by the European automotive system, which is different from the Silicon Valley model in the U.S. and the policy-driven market system in China. Volkswagen, for example, takes 50 months—more than four years—to develop a completely new vehicle from the initial planning stage to production, which is twice as long compared to some Chinese domestic brands, whose development time is around two years. This delay is naturally reflected in the slower pace of the entire electrification process.

It is worth mentioning that traditional European automakers are still making profits from their fuel-powered vehicle businesses, while their electric vehicle (EV) operations are currently in a loss-making state. The strong reputation and profitability of fuel-powered cars, built over years of history, have made it difficult for European automakers to let go of them. This psychological attachment has also contributed to the slow pace of their electrification process.

(Audi)

Currently, the distribution of charging stations and other infrastructure across Europe is extremely uneven, and the government has not implemented a unified plan for their installation. Electric vehicle (EV) users also do not have convenient access to charging options. According to the latest data, the number of public and semi-public charging stations in Europe exceeds 900,000, with the Netherlands, Germany, and France having the most charging stations, together accounting for more than half of the total number of charging stations in Europe. However, the distribution of charging stations in Europe is highly uneven. Some countries, such as Belgium and Finland, have seen significant growth rates in the past year and a half, reaching 190% and 158% respectively, but there are still large rural and remote areas that lack sufficient charging infrastructure. This uneven distribution limits the adoption of electric vehicles in these regions and hinders the overall progress of the energy transition.

(Tesla charging piles)

4. Conclusion

The electrification of the automotive industry in Europe is bound to be a challenging journey. The high costs of transformation, the complexity of the supply chain, and the deeply ingrained traditional mindset pose significant obstacles for European automakers. However, crises often come with opportunities. Europe's strong industrial base, technological prowess, and commitment to environmental protection provide a solid foundation for the shift to electric mobility. Only by actively confronting these challenges and seizing opportunities can the European automotive industry find its position in the new competitive landscape.

If any infringement occurs, please contact us for deletion

Popular Cars

Model Year

Car Compare

Car Photo